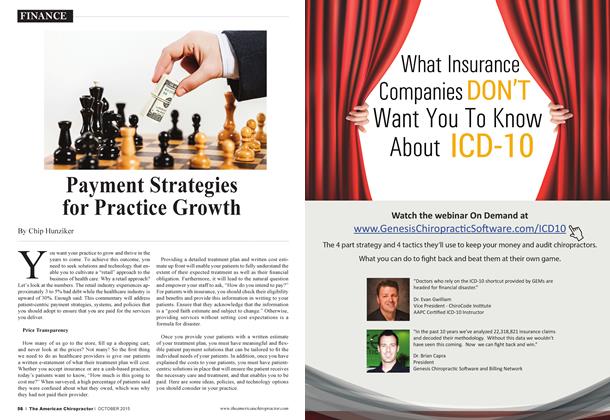

I t is estimated that with the rising popularity of consumer directed healthcare and the introduction of the Affordable Care Act ("Obama Care"), patient out-of-pocket healthcare expenses will reach almost $500 billion by the year 2015. As a result, healthcare providers are experiencing a dramatic increase in patient bad debt and declining revenue as patients forgo or abbreviate their care due to limited or no healthcare benefits, higher co-pays and large deductibles. Consider these chilling statistics: 51% of patients seeking chiropractic care chose not to receive treatment or abbreviated their care due to finances.' Chiropractors collect only 72% of their expected revenue.2 • 37% of Americans say the lack of financing options is why they do not get the care they need.' Adopt a "Rctail-ish" Approach to Healthcare What can you do to help patients overcome their cost concerns and help them move forward with the care they want and need? Cultivate a "retail" approach to the business of healthcare. Wal-Mart. Toy-R-Us. Best Buy. Home Depot and other successful retailer"s do it. Yes. what I am talking about is the "f" word - financing. By providing your patients with ways to finance the care they need, you can increase practice revenue, enhance cash How and. more importantly, help more people live pain free and productive lives. Lct"s explore some practical approaches for introducing patient finance options into your practice. "To be or not to be the bank? That is the question!" There arc typically two different approaches to providing patient financing. You can offer financing through a financial institution, an approach that involves introducing your patient to a third-party who provides them (or you) with cash to pay for your sen ices. Or. you can choose to finance your patients yourself, in which case your practice serves as "the bank." and in exchange for what amounts to an "IOU" from the patient, you provide sen ices with the expectation of being paid over time. Both options will result in higher conversion rates and utilization of sen ices by enabling your patients to pay for services overtime in smaller amounts that fit within their budget. However, determining which option might be the best choice for your practice depends on a variety of different factors, including your patient demographics, your individual needs, the charges and costs of your treatments and the capabilities of your practice. Lets take a closer look at both options. Third-Party Patient Financing The major advantages of third-party financing arc enhanced cash flow and a reduction of bad debt as the lender assumes the risk related to patient non-payment. Depending upon the lender, you may receive a lump sum payment upfront or a notification of a patient's "credit line" which you can bill against as sen ices arc rendered. Additionally, because your staff is not responsible for managing the collection process, it reduces your administrative burden allowing your staff to focus on patient care rather than chasing down patients for payments. When evaluating a third-parry provider, consider the following: • What arc the patient acceptance criteria? Most third-party finance companies require a credit check, and in today's economy mam patients arc reluctant to have their credit checked or won't qualify. Will the majority of your patients qualify? If not. win bother? • Is the lender patient (practice) friendly? The experience your patients have with your third-parry vendor is just as important as the one they have in your exam room. Be sure the lender's commitment to customer sen ice and patient satisfaction mirrors what you practice in your office. Is the application process and documentation required onerous, invasive, or time consuming? Is approval instantaneous? Docs your staff have to overnight mail or fax documents? • The devil is in the detail. Beware the fine print and review the interest rates and terms the patients must adhere to. Choose a vendor that you would be willing to use if you or a family member required it. Docs the lender require significant down payments and/or large monthly payments? If the patient needs to change their payment amount or miss a payment, arc there retroactive or punitive interest rates or penalties applied? • What are the costs to your practice? With third party lending you get the cash in hand quickly with littlc-to-no bad debt. However, payments will often be at a "discount." You have to know your costs. If your practice currently offers discounts (insurance companies, prc-pay or limited benefit plans) you should compare these to the discounts offered by the lender. How do they compare? Remember, you arc offering your patients a payment plan in lieu of a discount and I strongly encourage you to never discount a payment plan! In-Housc Patient Financing The big advantage to in-house financing is you have complete control over the patient experience, whether or not to offer financing, and under what terms. Additionally, providing "patient payment plans" while requiring you to wait for your payments, enables you to build recurring revenue as payments will be made to you over time. Here are some tips to think about when considering serving as the bank: • Do \ou have the right people and policies in place? Decide whether you want your staff or a billing company to administer your portfolio of "loans." If you choose to self-administer, your staff must have the available time and disposition to diligently manage any declines, changes, cancellations and any complaints that may arise. And. you must make the time to oversee your staffs performance and hold them accountable. Do you have the right people in place and do they have the required disposition and time to manage this process? (Most "care givers" make terrible billcrs.) If you elect to use a billing company, arc their fees performance-based? • Should you have a written agreement with every pa tient? Yes! And the agreement should describe the procedures you will be delivering, the units and the cost of each and the total expected treatment cost. The agreement should include an explanation of your refund or cancellation policy and describe any related fees. The agreement should be signed and retained by each party. Do you have a written agreement and is it in compliance with state, federal regulations and board guidelines related to installment plans? • Do you know your costs? "More is better than less." and if vou choose to be the "bank." you must think like a "banker" and manage your risk appropriately. You need to understand your cost structure by modality and how your costs change throughout the duration of care. Most care plans arc "front loaded" where the provider incurs the cost and the patient receives most of the services in the early (acute) phase of the treatment plan. Patients who receive hundreds of dollars in non-refundable supplements or medical equipment upfront should be required to pay a significant down payment versus those who do not. You should adjust your down payment requirements accordingly. Do you have a thorough know ledge of your cost structure by therapy and modality? Sooner is better than later. We have all heard the phrase "time is money." Don't kid yourself, if you arc offering payment plans, your practice is incurring the cost of money, which includes any "bad debt." and these costs equate to a "discount." Payment plans that run three, six or twelve months all have different costs and various degrees of increasing risk. Keep the payment term as short as possible (and ideally) timed to coincide with the end of the patient's treatment plan. Will you establish strict payment term guidelines? How and who in your office will be authorized to make exceptions? Will you use a collection agency for patients who ultimately default? Utilize technology and automate whenever possible. If you do not already, you should utilize a system that automates the recurring payments process. Make sure the system you use is payment card industry compliant (PCI). Accepting postdated checks or writing down your patient's credit card information and charging them later is likely a breach of Pay ment Card Industry ("PCI") Security Standards, and fines for this behavior arc catastrophic and can total $250,000 per incident. Additionally, you should never fax or email to any person or entity a patient's full credit card number. Conclusion "to be or not to be" For your practice to survive the days and years to come when, with or without insurance, most patients arc required to pay for most if not all of their care. You must adopt a retail approach to the business of healthcare. Be prepared for what to do when patients cannot pay for your recommended treatment plan at the time of sen ice. We discussed two options here, but there arc main solutions available in the market today to help your patients afford and pay for the care they need. These solutions may consist of companies that you can partner with that provide a blended solution as "one size does not fit all." Regardless of the programs or solutions you choose, with a well thought-out "finance" program in place and a staff that is educated on how and when to offer financing, you and your patients will be much better off in the days and years to come. Reference: The Effect of Cost Sharing on the Use of Chiropractic Sen ic es. Department of Veterans Affairs Medical Center. Sept 1996 A Rising Tide. Chiro Economics May 2013 The Next Wave of Change for US Healthcare payments, McKinscy&Coinpany May 2010 Chip Ilunziker, is the founder andC 7sO ofC learGage, Inc. a leading provider of patient payment and financial solutions to the Chiropractic market. Chip has over 25 years of experience in the health care, financial services and employee benefits industries. He can be contacted at 888-227-5932, info'a,cleargage.com or www.cleargage.com.